When it comes to property investment, one of the biggest decisions you’ll face is whether to focus on cash flow or capital growth. Both strategies have their advantages, but choosing the right one depends on your financial goals, risk tolerance, and investment timeline.

At Lagos Financial, we specialise in helping Australian property investors navigate these choices with confidence. In this guide, we’ll break down the differences between cash flow and capital growth strategies, discuss their pros and cons, and provide tips to help you decide which path aligns best with your goals.

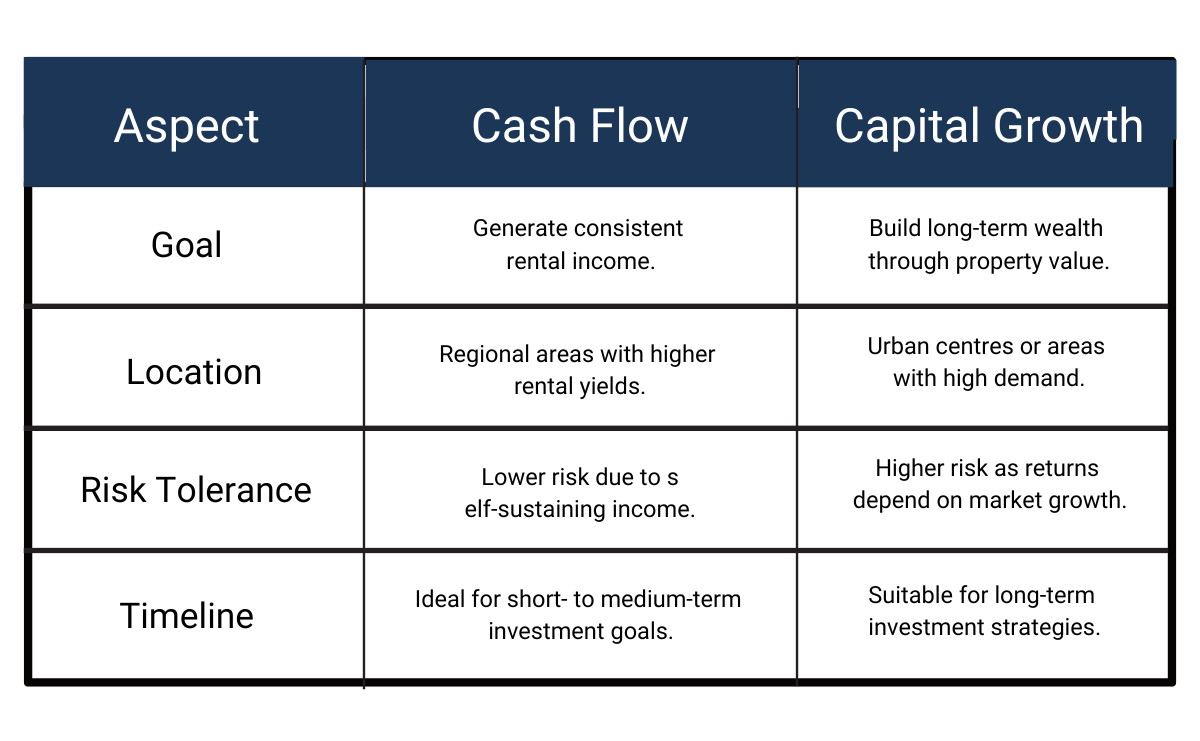

What Is Cash Flow?

Cash flow refers to the net income generated from your investment property after accounting for all expenses, such as loan repayments, maintenance costs, and property management fees.

A positive cash flow property is one where the rental income exceeds the expenses, providing you with consistent income each month.

Key Features of a Cash Flow Strategy:

- Focus: Steady, immediate rental income.

- Target Properties: Often found in regional or high-yield areas.

- Risk Level: Lower, as the property can sustain itself financially.

What Is Capital Growth?

Capital growth refers to the increase in the property’s value over time. Investors pursuing this strategy aim to sell the property at a significantly higher price than the purchase cost, building long-term wealth.

Key Features of a Capital Growth Strategy:

- Focus: Long-term property appreciation.

- Target Properties: Typically located in metropolitan areas or growth corridors.

- Risk Level: Higher, as the property may rely on market conditions rather than immediate income.

Cash Flow vs. Capital Growth: Key Differences

The Pros and Cons of Each Strategy

Cash Flow Strategy: Pros

- Steady Income: Regular rental income can help cover loan repayments and boost cash flow.

- Lower Risk: Positive cash flow properties are less likely to strain your finances.

- Portfolio Expansion: Extra income can be reinvested into additional properties.

Cash Flow Strategy: Cons

- Limited Growth Potential: Properties may not appreciate significantly in value over time.

- Location Dependence: Often found in regional areas with lower demand.

- Tax Implications: Positive cash flow is subject to income tax.

Capital Growth Strategy: Pros

- Significant Wealth Creation: Long-term value appreciation can lead to substantial profits.

- Strong Demand: Properties in high-growth areas often attract tenants and buyers.

- Equity Building: Increased property value can be leveraged for further investments.

Capital Growth Strategy: Cons

- Higher Risk: Returns depend on market performance and may fluctuate.

- Negative Cash Flow: Many growth-focused properties require financial support to sustain.

- Longer Timeframe: Benefits are realised over years or even decades.

How to Choose the Right Strategy

1. Assess Your Financial Goals

- If you’re looking to build immediate income or achieve financial independence sooner, a cash flow strategy may be ideal.

- If you’re planning for retirement or long-term wealth, focus on capital growth.

2. Consider Your Risk Tolerance

- If you prefer a lower-risk approach that doesn’t heavily rely on market performance, opt for cash flow.

- If you’re comfortable with potential market fluctuations for greater long-term rewards, consider capital growth.

3. Evaluate Your Borrowing Capacity

- Cash flow properties can enhance your borrowing capacity through additional rental income.

- Capital growth properties may require a strong financial buffer to handle higher expenses.

4. Think About Location

- For cash flow, look at suburbs with higher rental yields, such as regional areas or emerging markets.

- For capital growth, target metropolitan areas or suburbs with infrastructure growth and strong demand.

Can You Combine Both Strategies?

Absolutely! Many successful property investors adopt a balanced approach, combining properties that deliver cash flow with those positioned for capital growth. For example:

- Cash Flow Property: A unit in a regional area providing positive rental income.

- Capital Growth Property: A house in a growth corridor with long-term appreciation potential.

This strategy allows you to enjoy steady income while building long-term wealth.

Real-Life Example

Let’s look at two scenarios:

- Cash Flow Property:

- Purchase Price: $300,000

- Gross Rental Yield: 6% ($18,000/year)

- Net Cash Flow After Expenses: $4,000/year (positive cash flow).

- Capital Growth Property:

- Purchase Price: $700,000

- Annual Growth Rate: 6% ($42,000/year).

- Net Cash Flow After Expenses: -$5,000/year (negative cash flow).

Both investments have their benefits. The key is understanding which aligns better with your goals.

Work with an Experienced Mortgage Broker

Choosing between cash flow and capital growth doesn’t have to be a daunting task. At Lagos Financial, we take the time to understand your financial goals, risk appetite, and investment timeline. Our tailored solutions and expert advice help Australian property investors make confident decisions.

Conclusion: Your Investment Journey Starts Here

Understanding the difference between cash flow and capital growth is essential for creating a successful property investment strategy. By assessing your goals and financial position, you can decide which approach – or combination – works best for you.

Related Reading

- Property Investment Finance — Learn about our tailored investment loan solutions

- Understanding the Difference Between Cash Flow and Capital Growth in Property Investment

- Using Leverage to Grow Your Wealth: Strategies for Debt and Investment

- How to Maximise Borrowing Capacity for Property Investments

- Types of Investment Strategies

- Guide to Rental Yields

Ready to discuss your investment strategy? Book a complimentary assessment with our team.

Ready to take the next step?

Download our FREE Ultimate Property Investor’s Blueprint for detailed insights into investment strategies and how to grow your portfolio.

Victor Lagos

Founder & Mortgage Broker, Lagos Financial

Victor Lagos is a licensed mortgage broker and property investment strategist. As founder of Lagos Financial, he helps Australians build wealth through tailored finance solutions, working with 60+ lenders nationwide. He also hosts the Debt to Financial Freedom podcast.

Book a Free Assessment →